Balanced Strategy as at 31 December 2024

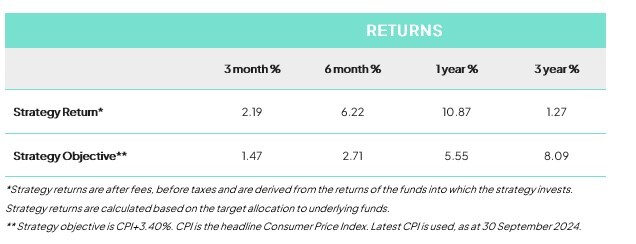

The Aurora Balanced Strategy continued to deliver positive returns across all measured periods, exceeding its CPI+ benchmark over the quarter, 6-month, and 1-year timeframes. This strong performance reflects the benefits of a diversified portfolio in a quarter where markets showed mixed results.

Global equities were the standout contributor to the strategy's returns. Unhedged global equities posted an impressive 12.4% gain for the quarter, benefiting from a strong US dollar. However, currency-hedged global equities recorded a more subdued 1.2% quarterly gain.New Zealand equities also delivered robust gains, rising 5.5% for the quarter and 11.9% for the year. This was supported by improving business and consumer confidence, on the back of Reserve Bank of New Zealand continuing to lower the Official Cash Rate, to 4.25%.

Conversely, listed infrastructure detracted from performance, declining 7.1% for the quarter as rising bond yields and a higher-rate environment weighed on valuations. Global bonds also faced challenges, falling 1.2% as central banks signalled a slower pace of rate cuts in the face of persistent inflation pressures.

The strategy's positive results underscore the importance of maintaining a diversified portfolio. While some asset classes, such as infrastructure, faced headwinds, the strong performance of global and New Zealand equities helped the strategy deliver on its objectives.

As we enter 2025, markets will face a range of challenges. Persistent inflation is likely to keep the Federal Reserve cautious, slowing the pace of rate cuts and maintaining elevated bond yields, which could pressure both equity and fixed-income markets. U.S. stock valuations remain stretched, limiting the potential for further upside, particularly if earnings fail to meet high expectations. Deglobalisation trends, driven by increasing tariffs and trade tensions, may disrupt supply chains and dampen global trade which could add to market volatility. Meanwhile, New Zealand’s gradual recovery, supported by ongoing rate cuts, offers a brighter outlook for domestic equities.