Recent changes to KiwiSaver legislation mean that from 1 April, minimum employee and employer contributions have increased from 3% to 3.5%, and will rise again to 4% in April 2028.

While these changes might seem small, they can have a big impact on your KiwiSaver balance over the long term – thanks to the power of compounding returns.

Compounding is often compared to a snowball rolling down a hill, gathering more snow as it moves. In a savings account, you earn interest on your initial deposit; if you leave that interest in the account, you then earn interest on both the original sum and the interest already earned.

With a KiwiSaver account, the process is similar but involves investment returns. These returns – which may include dividends, capital gains, or interest – are reinvested into your fund. Over time, you have the potential to earn returns on your previous returns.

It’s easy to dismiss a 0.5% or 1% increase as something that won’t really move the needle on your future. But compounding returns thrive on exactly these small, consistent changes – so making small changes now can have a big impact in the future. Here’s what that looks like in action.

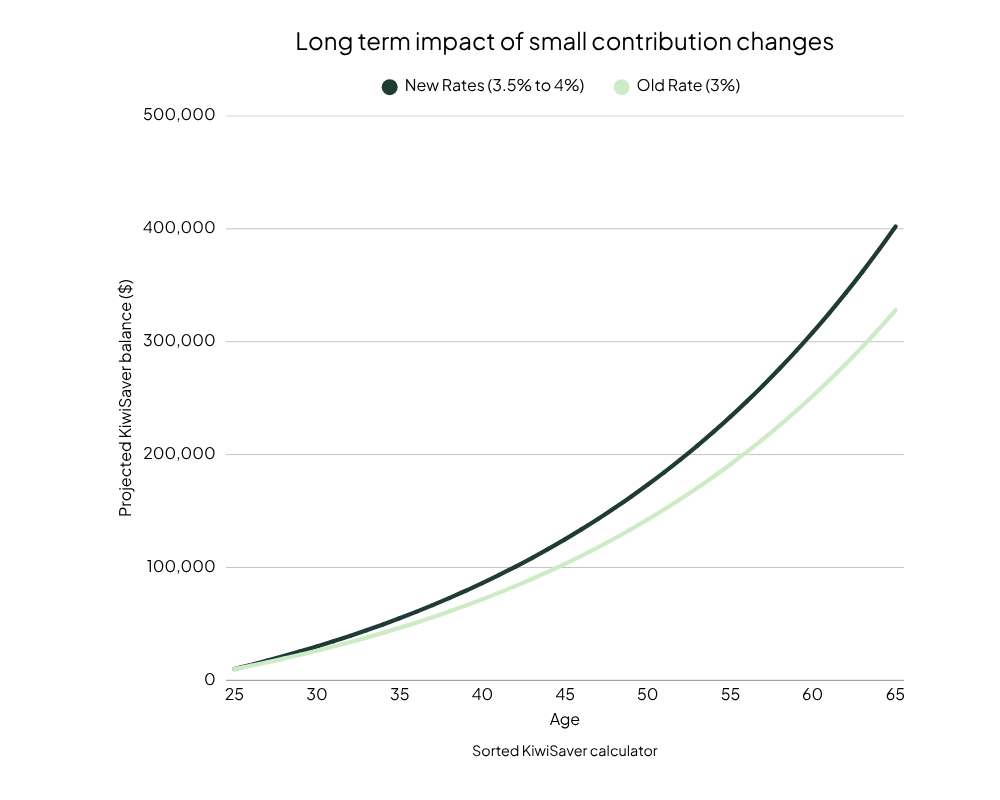

Eloise is a 25 year old who earns $60,000 and has $10,000 invested in a growth fund in her KiwiSaver account. Although the new KiwiSaver contribution rate changes may seem small, Eloise has a further 40 years until she can access her KiwiSaver money for retirement – plenty of time to take advantage of compounding returns.

If Eloise continues contributing at the minimum employee contribution rate (currently 3.5% and moving to 4% on 1 April 2028) she could have close to $402,000 at age 65.

If the minimum contribution rate had stayed at 3%, Eloise’s KiwiSaver balance at 65 would have been closer to $328,000 – that’s a huge $74,000 more to go towards the lifestyle she wants in her retirement.

Figures calculated using the Sorted KiwiSaver calculator

Compounding is most effective over long periods, which is why starting early can be a key factor in enjoying the lifestyle you want in retirement. It’s important to remember though, that KiwiSaver is an investment and returns are not guaranteed. They can be positive or negative depending on market conditions, and your balance will fluctuate.

By staying invested through these fluctuations, you allow compounding the time it needs to potentially grow your savings for your retirement.

Talk to your Adviser today or get in touch with the Aurora Client Care Team

0800 242 023

hello@aurora.co.nz