KiwiSaver has become one of New Zealand’s most important financial tools — with over $140 billion saved by 3.4 million members* — it’s the main way most of us are saving for retirement. Yet a surprising number of us aren’t getting as much out of it as we could, based on beliefs about KiwiSaver that simply aren’t true.

Here are six of the most common myths — and the reality behind each one.

*Source: IRD & RBNZ.

This is probably the most expensive myth on this list.

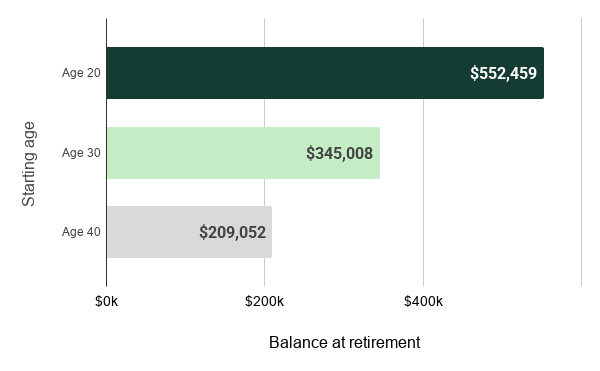

The single biggest factor in how much you end up with at retirement isn’t how much you earn, or even how much you contribute — it’s how long your money has to grow. Someone who starts contributing at 20 could end up with around $552,000 at retirement. Wait until 30 and that drops to around $354,000. Start at 40 and you’re looking at roughly $209,000. Same salary, same contribution rate, same fund — just a different starting age.

How your starting age affects your retirement balance

Source: Sorted KiwiSaver calculator. Example based on an investor with a starting salary of $75,000; invested in a growth fund and a zero starting balance.

That gap exists for two reasons. The first is simply time — starting earlier means more years of contributions flowing in from you, your employer and the government. The second is compounding. Your contributions earn returns, and those returns earn returns of their own. Together, these two forces mean that the money you put in during your 20s does far more heavy lifting than the same dollar contributed in your 40s.

NZ Super is a foundation, but it’s not a retirement plan on its own.

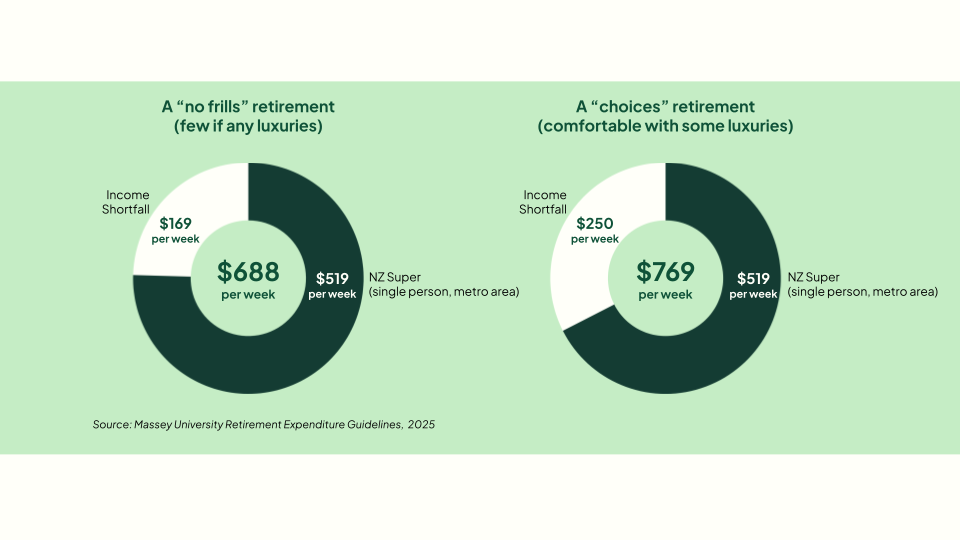

According to Massey University’s Retirement Expenditure Guidelines 2025, a single person in a metro area needs around $688 per week for a basic “no frills” retirement. NZ Super currently provides $519 per week, leaving a shortfall of $169 every week. If you’re hoping for a retirement with some more choices — travel, treating the grandkids, not sweating every bill — the gap blows out to $250 per week.

That’s a lot of ground to cover. KiwiSaver is designed to help bridge it. The more thought you put into your settings now, the better placed you’ll be to close that gap and enjoy the retirement you’re working towards.

The minimum gets you started — but it may not get you where you want to be.

From April 2026, the minimum employee contribution rate increased from 3% to 3.5%, with a further increase to 4% coming in 2028. These changes will help, but the minimum is still just a floor, not a target.

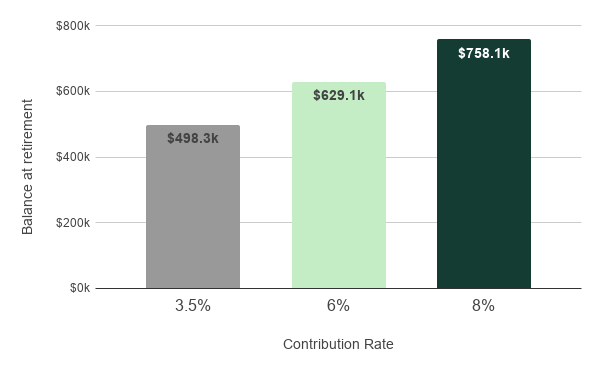

The difference between contributing the minimum or contributing a little more can be surprisingly significant over time. Take someone aged 25 with a current balance of $20,000 and a salary of $75,000 invested in a growth fund. Increasing their contribution rate from 3.5% to 6% could add around $131,000 to their balance by retirement. Push that to 8% and the difference grows to almost $260,000. That’s not a small number.

How your contribution rate affects your retirement balance

Source: Sorted KiwiSaver calculator.

Even a small increase in your contribution rate today, combined with time and compounding, can make a meaningful difference to the retirement you’re able to enjoy.

They’re really not — and the difference matters more than most people realise.

KiwiSaver funds range from cash and conservative options through to balanced and growth funds, each with different types of underlying investments, different levels of risk, and different long-term return potential. The right fund depends on your goals, your timeframe, and your comfort with ups and downs.

To put some numbers on it: on the same salary with the same contributions, someone in a conservative fund could retire with around $327,000. Someone in a growth fund could retire with around $498,000*. The fund you’re in today could shape what your retirement looks like in the future.

For younger members with decades of investing ahead of them, being in the wrong fund type is one of the most common and most fixable KiwiSaver mistakes. If you’ve never actively chosen your fund and were automatically signed up through work, it’s worth checking which fund you’re actually in.

*Source: Sorted KiwiSaver calculator. Example based on a 25 year old investor with a starting salary of $75,000, a KiwiSaver balance of $20,000, making minimum contributions and invested in a growth fund.

This is one of the most common — and costly — KiwiSaver mistakes people make.

When markets fall and headlines turn negative, switching to a conservative fund feels like the sensible thing to do. But by the time most people make that call, the drop has already happened. You’ve locked in your losses at the bottom, and when markets recover — as they historically always have — you’re no longer invested to benefit from the rebound.

For younger members, market downturns are a normal part of long-term investing. Your balance will dip from time to time. That’s not a crisis — it’s just how markets work. What matters is staying invested and giving your money the time it needs to recover and grow.

If you find yourself tempted to make a change when markets are rough, that’s a good moment to talk to an adviser rather than act on instinct.

KiwiSaver is designed to be low-effort, and that’s genuinely one of its strengths. If you’re employed, contributions come out of your pay automatically, you don’t have to think about it, and it just runs.

The problem is when “easy” becomes “ignored.” The settings that made sense when you were 22 may not be right for you at 32 or 42. Life changes — income may increase, goals can shift, a relationship could change your financial picture. Your KiwiSaver account settings should keep up.

There’s also a behavioural upside worth knowing about. When contributions come out automatically the moment your pay lands, most people genuinely don’t notice the money is gone. No willpower required, no monthly decision, no temptation to spend it instead. That’s a feature, not a bug — but it only works in your favour if the settings are right in the first place.

KiwiSaver doesn’t need to be complicated. But “simple” and “sorted” aren’t the same thing.

According to FSC research, only 44% of New Zealanders feel prepared for retirement. For most of us, getting there isn’t about dramatic financial overhauls — it’s about making a few good decisions early and revisiting them as life changes.

If any of these myths have felt familiar, it could be worth having a conversation with an adviser to make sure your KiwiSaver account is set up in a way that works for you.

Your future self will thank you for the effort.

Want to talk things through?

Talk to your Adviser today or get in touch with the Aurora Client Care Team

0800 242 023

hello@aurora.co.nz

Projections referenced in this article are from the Sorted KiwiSaver Calculator. Actual returns will vary and are not guaranteed. This article provides general information only and is not personalised financial advice. For advice specific to your situation, please speak with your Financial Adviser.