Buying your first home is one of the biggest financial steps you’ll take, and if you’re a KiwiSaver member, you’re already ahead of the game. At Aurora, we’ve helped nearly 900 members step onto the property ladder, paying out close to $28 million* from their KiwiSaver investments to make homeownership a reality. We understand that entering the property market can feel overwhelming, but your KiwiSaver account could provide the extra boost you need to take that exciting first step.

Let’s break down how KiwiSaver can help make your homeownership dream a reality.

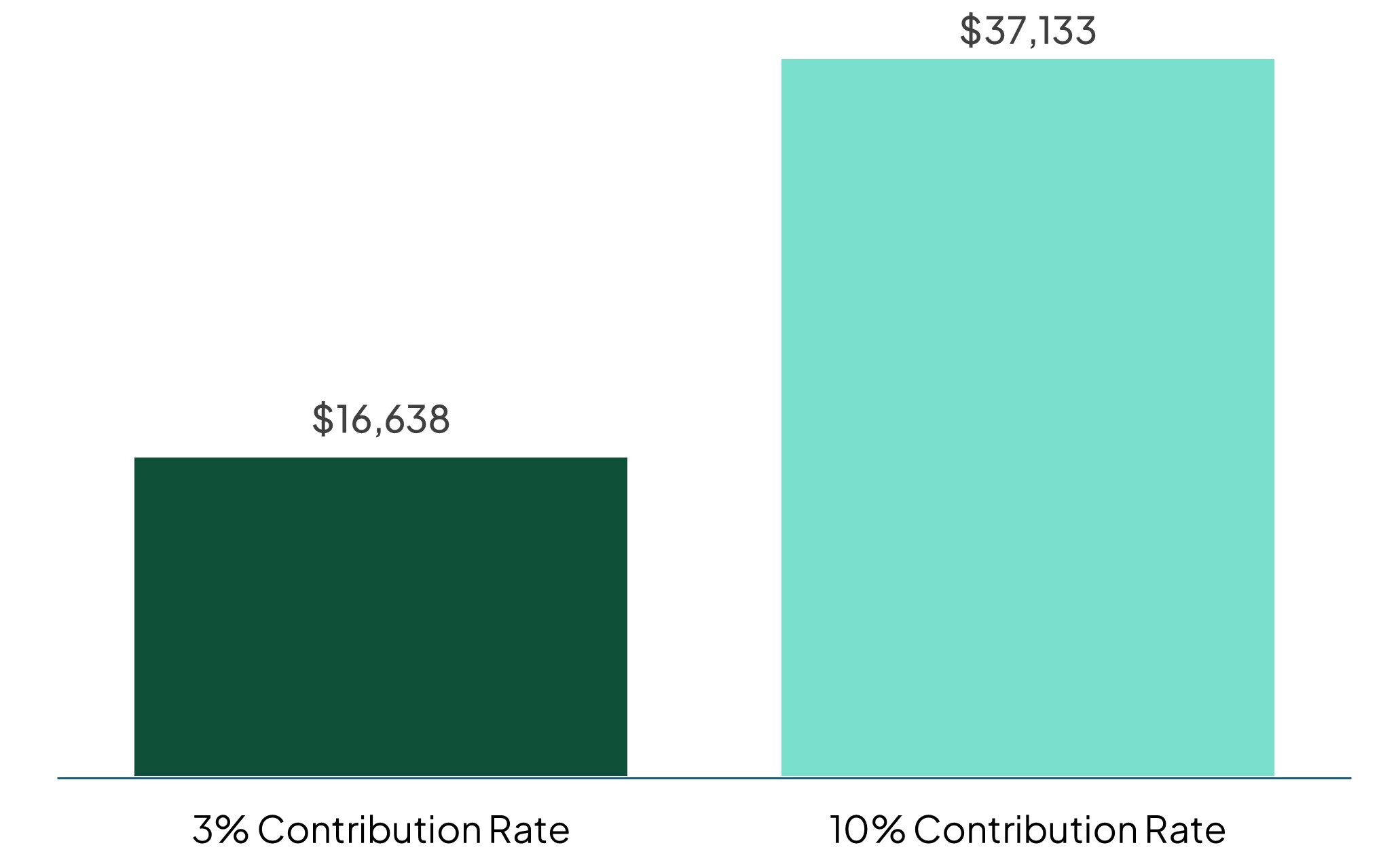

Firstly, the more you contribute to KiwiSaver, the larger your deposit will be, and the less you’ll need to borrow for your mortgage. Now is the time to ramp up your savings. A simple step like increasing your contribution rate can make a significant difference to your KiwiSaver balance over time.

The default contribution rate is 3%, however you can choose from 4%, 6%, 8% and 10%. Sarah is 25 years old and earns $50,000 per year. Check out the example below where she decides to increase her contribution rate from 3% to 10% for five years.

Figure 1. Sarah’s pumped! Ramping up her contribution rate to 10% has increased her expected account balance

Includes government and employer contributions. Based on a Conservative Fund with an average annual return of 2.5%, after fees and tax. Adjusted for inflation currently assumed to be 2%.

It’s important to ensure that the fund you’re invested in matches the timeframe for when you plan to access your savings to buy your first home. An Aurora KiwiSaver adviser can guide you in choosing the right fund, as different types come with varying levels of investment risk. As you approach your withdrawal date, it’s smart to switch to a fund with lower volatility, so your investment is better protected from potential market downturns. We offer a range of investment options tailored to your risk tolerance and timeframe.

If you’re planning to access your KiwiSaver investment within one to three years, our First Home Buyer Strategy could be the perfect fit for you. This strategy aims for stable returns by investing in mainly income assets, with some investment in growth assets. This allows you to better safeguard your investment while keeping you on track for your homeownership goal.

If you’ve been contributing to KiwiSaver for at least three years, you might be able to withdraw most of your savings to put towards your first home.

You can withdraw nearly everything in your account – your contributions, your employer and government contributions, and any investment returns. The only catch is that you’ll need to leave at least $1,000 in your KiwiSaver account. Also, if you have transferred any funds from an Australian Complying Superannuation scheme, those funds are unable to be withdrawn.

Download our handy First Home Buyers Checklist for more information.

While using your KiwiSaver investment for your first home can be a great way to get ahead, it’s important to remember that withdrawing money from your account means you’ll be starting again to save for your retirement. After buying, it’s smart to review your KiwiSaver contributions and fund type to make sure it matches your new financial situation and retirement goals.

We’re here to help you make the most of your KiwiSaver investment, whether it’s for your retirement or buying your first home. If you’re ready to take the leap into homeownership, using KiwiSaver and our First Home Buyer Strategy investment option could give you the leg-up you need. Get in touch with us, and we’ll help you get started on making your dream home a reality.

*As at 22 November 2024

DISCLAIMER

This information is provided in a general nature only and should not be construed as or relied on as financial advice. This is not a recommendation to invest in a particular financial product or class of financial products. You should seek financial advice specific to your circumstances from a Financial Adviser before making any investment decisions.

Past performance is not a reliable indicator of future performance. The value of your investment may go up and down.